October Forecast for 2017 Corn Production Higher than Last Month

Author

Published

10/20/2017

The USDA released the October report of the World Agricultural Supply and Demand Estimates (WASDE, October 12, 2017), forecasting higher 2017/18 corn production, increased corn use for both feed and residual and food, seed and industrial (FSI) (excluding corn for ethanol use). Corn ending stocks were marginally increased, and the 2017/18 corn price forecast remained unchanged from the September 2017 forecast.

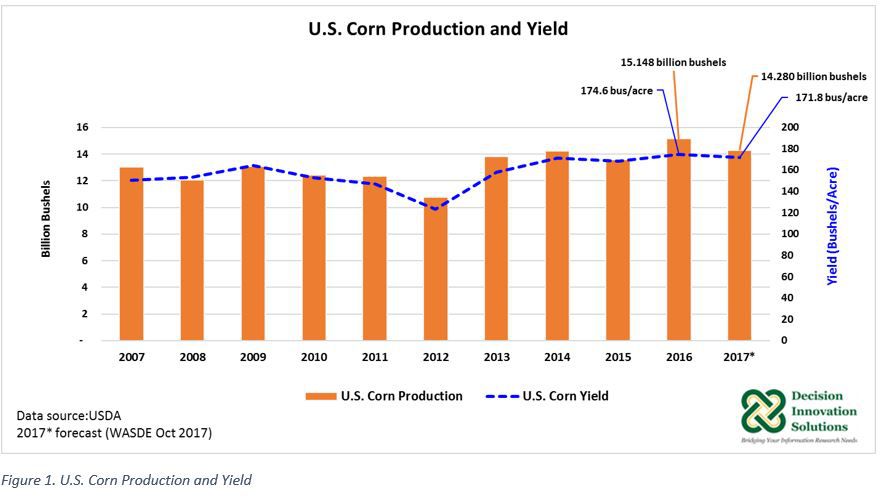

With corn yield forecast increased this month by 1.9 bushels/acre to 171.8 bushels/acre, 96 million bushels were added to estimated 2017 production, resulting in a forecast of 14.280 billion bushels of corn. If realized, U.S. farmers could achieve the second-highest yield and corn production on record after setting new records in 2016 (see Figure 1).

2017/18 beginning stocks (2016/17 ending stocks) were reduced by 55 million bushels to 2.295 billion bushels from last month's forecast (2.350 billion bushels) based on USDA updated Grain Stocks report published September 29, 2017. The quarterly corn stocks on September 1, 2017, were smaller than expected, yet they were the second largest since 1987/1988 (4.259 billion bushels).

2017/18 corn supplies were up by 40 million bushels to 16.625 billion bushels compared with the previous month's forecast (16.585 billion bushels). The latest corn supply forecast is down 317 million bushels from the 2016/17 marketing year estimate (16.942 million bushels).

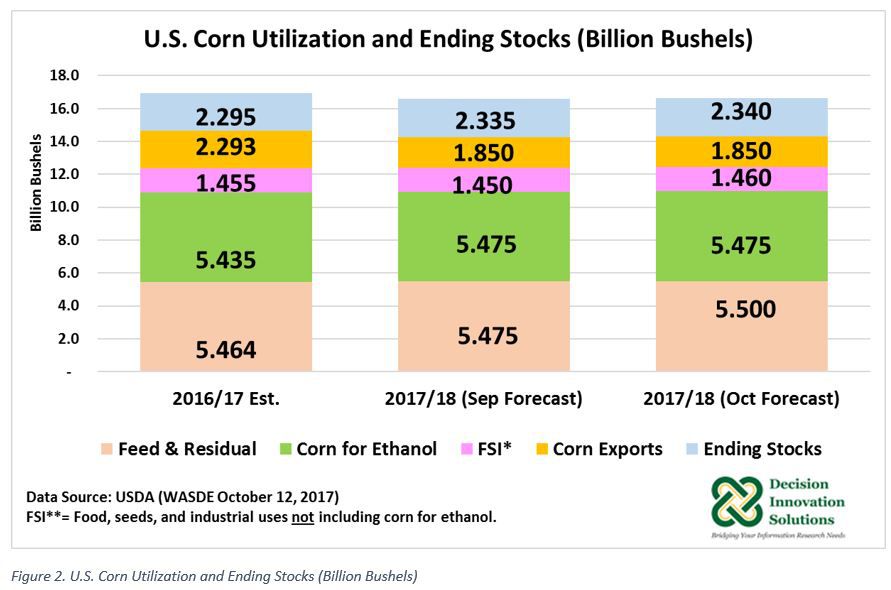

On the corn demand side, the October 2017 forecast for 2017/18 corn use for feed and residual was up 25 million bushels from last month's forecast to 5.500 billion bushels (see Figure 2). A large crop and low expected prices are boosting feed demand. If realized, this would be the largest corn used for feed and residual since 2007/08 (5.853 billion bushels). The October projection for 2017/18 corn for ethanol production (5.475 billion bushels) was unchanged from last month's projection but if achieved, it would be the largest on record. 2017/18 corn use for feed, seed, and industrial (not including corn for ethanol use) was up by 10 million bushels to 1.460 billion bushels from the previous month's projection (see Figure 2). Despite lower beginning stocks, due to the larger production and changes in corn use the latest forecast for 2017/18 total domestic corn demand was raised by 35 million bushels to 12.435 million bushels compared with last month's projection.

The October forecast for 2017/18 corn exports equaled 1.850 billion bushels. This forecast has remained the same since August 2017 when exports were forecast down 25 million bushels from the July 2017 forecast (1.875 billion bushels). Increased competitiveness of supplies in Argentina and Brazil and a low volume of new-crop outstanding sales have been keeping the 2017 export forecast at his level. This projection is 443 million bushels below the 2016/17 estimate (see Figure 2).

The October 12, 2017, Grain World Markets and Trade report from USDA-FAS indicates the 2017/18 global corn production forecast is up 0.6 percent to 40.896 billion bushels[1] from the previous month based on higher production forecasts for the U.S., Nigeria, and Canada. Based on USDA-FAS trade year[2] data, Argentina’s 2017/18 corn exports were forecast down 4 percent to 1.063 billion bushels compared with the September forecast. Nonetheless, Argentina’s 2017/18 corn exports are forecast up 15 percent year over year. The October 2017 forecast for Mexico’s 2017/18 corn exports was increased by 24 million bushels to 51 million bushels from last month, which according to USDA-FAS, is based on higher demand for non-GM white corn, mainly from African countries. With this update, Mexican corn exports are expected to remain the same as last year. The Brazil 2017/18 corn export forecast (1.417 billion bushels) remained unchanged from last month. If realized, Brazil 2017/18 corn exports would increase 82 percent relative to the 2016/17 trade year. Brazil is the largest U.S. competitor in the world corn market. Brazil’s second crop corn harvest by the end of the U.S. marketing year, is supporting Brazil corn exports during the September to January months.

The U.S. 2017/18 season-average farm price forecast in October is unchanged at $3.20 per bushel relative to last month projection. This price projection is down $0.41/bushel and $0.16/bushel from the 2015/16 and 2016/17 corn price estimate, respectively. Domestic and foreign demand for U.S. corn need to increase to boost U.S. corn price this year.

Want more news on this topic? Farm Bureau members may subscribe for a free email news service, featuring the farm and rural topics that interest them most!