Soybean tariffs could rock Iowa ag

Author

Published

4/9/2018

The Chinese Ministry of Commerce last week announced it would place tariffs on a number of U.S. goods in response to tariffs announced by the Trump administration. Specifically, the Chinese tariffs included a product that could rock Iowa agriculture: soybeans.

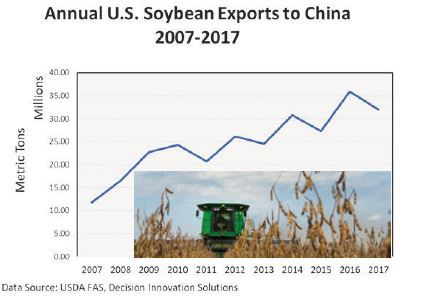

To understand the impact of these potential tariffs, let’s look at the last two years of soybean exports. It gives an idea of both the cyclical nature and magnitude of soybean exports to China from the United States.

Generally, at the peak of the export season during the months of September through March, exports can be as high as $3.5 billion exported in any given month. In 2016, exports to China for the year totaled $14.2 billion and in 2017, $12.4 billion. If tariffs had been added in these years, the cost of U.S. soybeans upon landing in China would have increased by $3.5 billion in 2016 and $3.1 billion in 2017.

Another way to look at this: If soybeans at the U.S. export port are trading about $10 per bushel, the imposition of a 25 percent import tariff by the Chinese government makes those same soybeans cost $12.50 per bushel to a Chinese crushing plant.

So the relevant questions are: If U.S. soybeans suddenly cost $2.50 per bushel more to Chinese users, what will their demand response be? Are there alternative supplies of soybeans available to Chinese importers? And to what extent will higher prices for U.S. soybeans cause Chinese crushers and feed users to substitute other sources of protein into their feed rations?

The answer to the first question is that Chinese users would not “quit using” U.S. soybeans simply because the price increases. However, it is likely that Chinese buyers would decrease their consumption, maybe by as much 10 percent.

The answer to the second question is yes, to a degree there are alternative supplies of soybeans. Brazil, which is now harvesting a record to near-record soybean crop, is already a major supplier of soybeans into China. China can purchase more soybeans from Brazil than they normally do, but there are limits to Brazil’s loading capacity.

The answer to the third question is that, in the long run, feed manufacturers and feed users in China can adapt to other protein and oilseeds. But that country’s crushing facilities tend to be set up for soybeans and not necessarily for other oilseeds. Also, the amino acid mix and nutritional values of substitute feeds are not exact matches for soybean meal. For soybean oil, there are more substitutes available to consumers, and consumers are not very price sensitive to soy oil prices at the household level.

Meanwhile, the impact of the potential Chinese tariffs on farmers in Iowa and around the United States would be complex, the result of many actions working simultaneously.

Yes, exports to China would decline, but some of those sales would be diverted to other destinations. Second, the world price of soybeans would likely decline modestly (likely 5 to 8 percent) and that decline could stimulate increased usage by non-China importers. Third, the impact would not be felt uniformly on the soy complex.

It is likely that world soybean meal prices could actually increase in response to less soy crush in China and less soy crush in the United States. Soybean oil prices would likely fall as substitute products are more likely to be available to Chinese consumers.

Tariffs are trade distorting, and most often, trade distortions are negative to world values of the underlying commodity products.

The U.S. Department of Agriculture projects that farmers will plant more acres of soybeans than corn in 2018. Those planting plans could change if a tariff further depresses soybean prices.

All of this should be understood within the context that these tariffs, as of now, are announced but not implemented. The implementation is pending trade discussions between the U.S. and China, to be completed in May 2018.

However, as we have seen in the pork market, and now the soybean market, talk of trade disruptions such as tariffs and retaliatory actions can and do move ag markets.

Our markets do not wait for actual government actions. They move on assertions, expectations, uncertainty, tweets, official statements and rumors of any of these. In my opinion, the current process of trade negotiations may work for manufacturing goods and financial products, but they can be quite damaging to agricultural trading systems and to farmers’ pocketbooks during the process.

Miller is the director of research and commodity services for the Iowa Farm Bureau Federation.

Want more news on this topic? Farm Bureau members may subscribe for a free email news service, featuring the farm and rural topics that interest them most!