NAFTA and U.S. Ethanol and DDGs Exports to Canada and Mexico

Author

Published

8/10/2017

The North American Free Trade Agreement (NAFTA) between the United States, Canada, and Mexico, established in 1994, has reduced barriers to trade and investment among the three North American countries. Trade between the United States and these two countries has significantly increased since NAFTA implementation. In 2016 Canada and Mexico were the second and third largest market for U.S. agricultural products, respectively. The value of U.S. agricultural product exported to Canada was equal to $20.5 billion in 2016, whereas U.S. agricultural exports to Mexico were valued at $17.9 billion. The largest market destination for U.S. agricultural products in 2016 was China, with $21.4 billion worth of U.S. agricultural exports.

U.S. Ethanol Exports

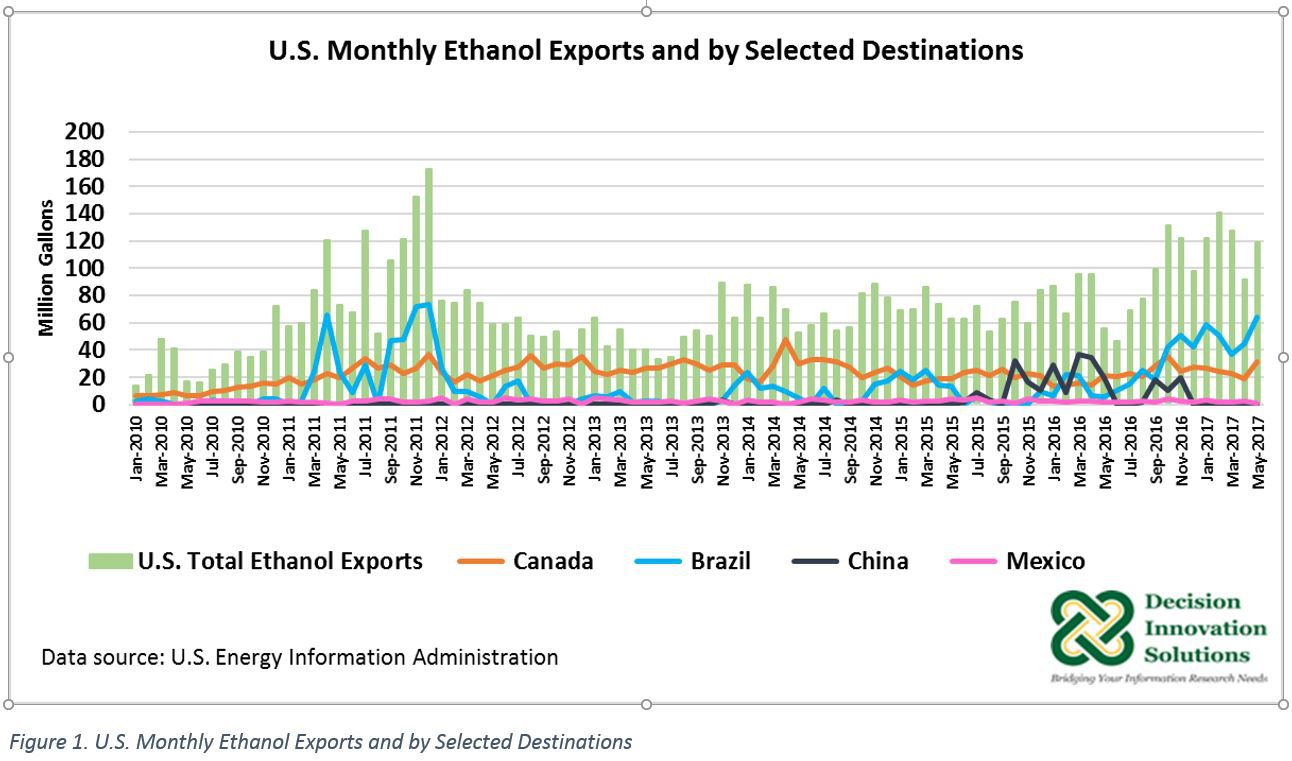

U.S. exports of ethanol have grown considerably since 2007 and Canada is one of the main market destinations for U.S. ethanol. In 2016, one quarter (259.3 million gallons) of total exports were shipped to Canada. Because of NAFTA, there is no tariff on renewable fuels produced in the United States and imported into Canada. After Brazil, Canada was the second largest market for U.S. ethanol in 2016. 2016 ethanol exports to Canada were up 3.1 percent compared with the previous year. Canada’s federal mandate is 5 percent of the national gasoline pool with some provinces having higher requirements. Saskatchewan and Manitoba, for instance have provincial mandates of 7.5 percent and 8.5 percent of the gasoline pool to be ethanol, respectively.

Mexico was the 8th largest market for U.S. ethanol exports, representing 2% (29 million gallons) of total U.S. ethanol shipments in 2016. Recently (June 2017), Mexico revised its biofuel law increasing the allowable amount of ethanol in gasoline from 5.8 percent to 10 percent. This regulation applies to the entire country except for the metropolitan areas of Mexico City, Guadalajara, and Monterrey. The new blending mandate intends to develop Mexico’s biofuel industry, where feedstocks such as sugar cane and sorghum are produced, but it also may increase opportunities to further expand U.S. exports to that country.

Overall, U.S. ethanol exports from January to May 2017 were up 49.9 percent to 601.104 million gallons compared with the same period in 2016. Canada continued as the second largest market for U.S. ethanol, with 20.7 percent of total exports (124.278 million gallons) and up 54.6 percent compared with January to May 2016. Canada is projected to import 264.2 million gallons of ethanol in 2017, which according to USDA-FAS, nearly 100 percent will originate from the United States. Brazil is the top market for U.S. ethanol so far this year (January to May 2017), with 42.5 percent (255.234 million gallons) of total U.S. ethanol exports (see Figure 1).

U.S. DDGs Exports

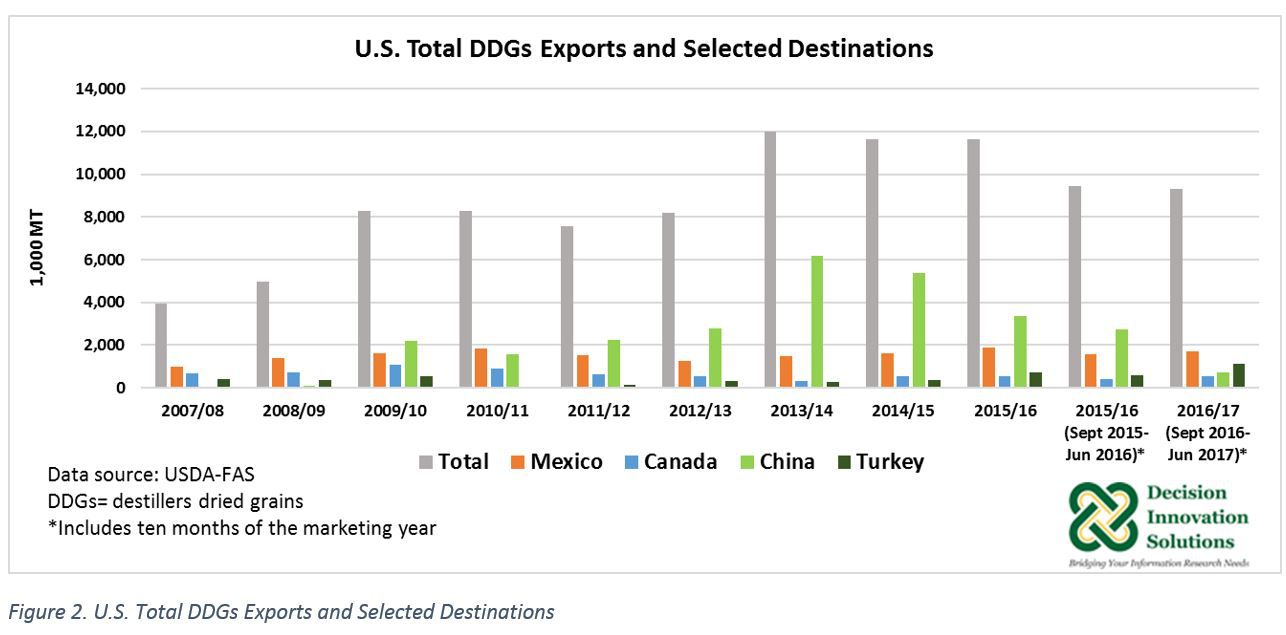

U.S. distillers dried grains (DDGs) exports have experienced a substantial increase mainly because of the significant increase in shipment to China, a country that from 2011/2012 to 2015/16 marketing years was the number one market for U.S. DDGs (see Figure 2). Despite China being the top market for DDGs in 2015/16, China’s antidumping and countervailing duty against DDGs coming from the United States reduced DDGs exports to that country during that marketing year. 2015/16 exports to China declined 37.7 percent to 3.342 million metric tons (MT) compared with the 2014/15 marketing year (5.366 million MT).

For the years that China has not been the top market for U.S. DDGs, Mexico’s imports have taken the lead (see Figure 2). U.S. DDGs exports to Mexico have been above 1 million MT since 2007/08, and in 2015/16 exports reached a volume of 1.9 million MT, increasing 19.4% from the previous marketing year. According to a recent publication (April 2017) Mexico Oilseeds and Products Annual report by USDA-FAS, the United States is the only source of DDGs to Mexico. Competitive DDGs prices over soybean meal prices is a factor that contributes to the strength of U.S DDGs exports to Mexico.

USDA-FAS data from September 2016 to June 2017 indicates Mexico is the number one market for DDGs with shipments reaching 1.689 million MT so far this year. Other important destinations during the first three quarters of the current marketing year are Turkey (1.107million MT), South Korea (0.846 million MT), the European Union (0.792 million MT), Thailand (0.686 million MT), Canada (0.548 million MT), Indonesia (0.392 million MT), Japan (0.344 million MT), and Other destinations (1.703 million MT). Mexico and these eight markets, have experienced growth compared with same period last marketing year. One of these eight markets include “Other destinations”, which has many markets embedded within it.

Exports to China and Vietnam, on the other hand, declined 73.5 percent to 0.722 million MT and 35.1 percent to 0.491 million MT, respectively. Despite large reductions in these two markets, particularly the Chinese market, total U.S. DDGs exports from September 2016 to June 2017 (9.322 million MT) have experienced a decline of only 1.1 percent compared with same period the previous marketing year (9.426 million MT) because of the growth in exports to Mexico and the other eight markets mentioned above.

NAFTA Modernization and Objectives Related to Agriculture

The United States free trade agreement with Canada and Mexico is on the verge of renegotiation (updated to reflect changes over the last twenty-three years). On May 18, 2017, notice regarding the modernization of NAFTA was provided to Congress by the U.S. Trade Representative Office (USTR) to fulfill the 90-day notice before initiating negotiations with any country (USTR, 2017). Public comments to help inform the direction and content of the NAFTA negotiations were closed on June 12, 2017. A public hearing was held on June 27, 2017.

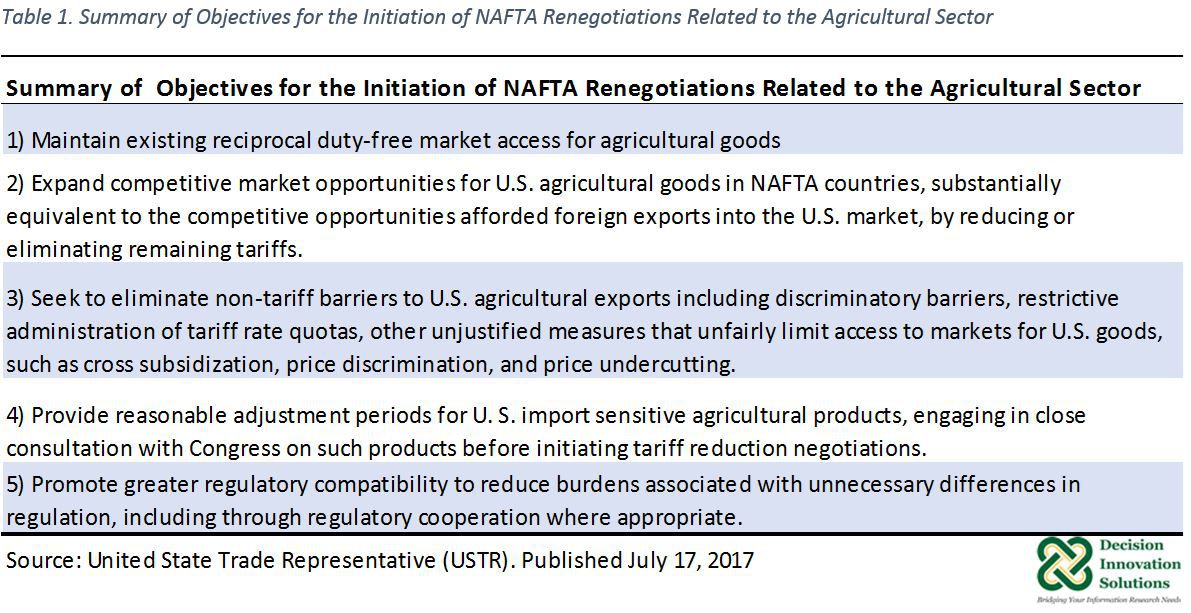

On July 17, 2017, the United States Trade Representative released NAFTA negotiation objectives. Page 4 of this document lists a summary of specific negotiating objectives for the initiation of NAFTA negotiations related to the agricultural sector (see Table 1). Objective 1 in particular offers some reassurance to U.S. ethanol and DDGs exports to Canada and Mexico. This objective indicates willingness to continue reciprocal duty-free market access for agricultural goods. The earliest date negotiations with Canada and Mexico can begin is August 16, 2017.

As the second largest destination for U.S. ethanol exports, Canada is an important market that greatly contributes to the strength of U.S. ethanol trade. Canada is the eighth largest market for U.S. DDGs exports. Currently, Mexico[1] is the top market for U.S. DDGs exports. In addition, Mexico’s new allowable ethanol blending into gasoline of 10 percent provides opportunities for expanding U.S. ethanol exports to that market. Renegotiation of NAFTA is intended to improve U.S. trade opportunities with Canada and Mexico but because NAFTA renegotiation results with these two countries is uncertain at this point, it is unclear what the impact on U.S. exports of ethanol and DDGs to Canada and Mexico would be. NAFTA renegotiations could begin as soon as August 16, 2017.

As the second largest destination for U.S. ethanol exports, Canada is an important market that greatly contributes to the strength of U.S. ethanol trade. Canada is the eighth largest market for U.S. DDGs exports. Currently, Mexico[1] is the top market for U.S. DDGs exports. In addition, Mexico’s new allowable ethanol blending into gasoline of 10 percent provides opportunities for expanding U.S. ethanol exports to that market. Renegotiation of NAFTA is intended to improve U.S. trade opportunities with Canada and Mexico but because NAFTA renegotiation results with these two countries is uncertain at this point, it is unclear what the impact on U.S. exports of ethanol and DDGs to Canada and Mexico would be. NAFTA renegotiations could begin as soon as August 16, 2017.

Note: Except for few updates, this report is based on an article originally published on July 13, 2017 by Iowa State University Agricultural Marketing Resource Center (AgMRC).

[1] Mexico has been the top market for U.S. DDGs exports so far this marketing year (September 2016 to June 2017), however, U.S. DDGs exports to “Other destinations” (1.703 million MT), which has many markets embedded within it, surpassed the volume of U.S. DDGs exported to Mexico (1.689 million MT) by 0.8 percent.

Want more news on this topic? Farm Bureau members may subscribe for a free email news service, featuring the farm and rural topics that interest them most!