U.S. Corn Export Sales are Lagging from Previous Two Years

Author

Published

2/22/2023

Due to lower planted acres and yield, 2022/23 corn production was estimated at 13.730 billion bushels, which was down 9% year-over-year. With lower corn production, corn usage projections, including corn exports, have been reduced compared with the previous year; however, as indicated in the latest WASDE report, the share of corn for domestic usage, in particular corn for ethanol, relative to total production, is expected to increase from 35% during last marketing year to 38% in the current marketing year. In contrast, the share of corn exports is expected to decline from 16% during the previous marketing year to 14% this marketing year.

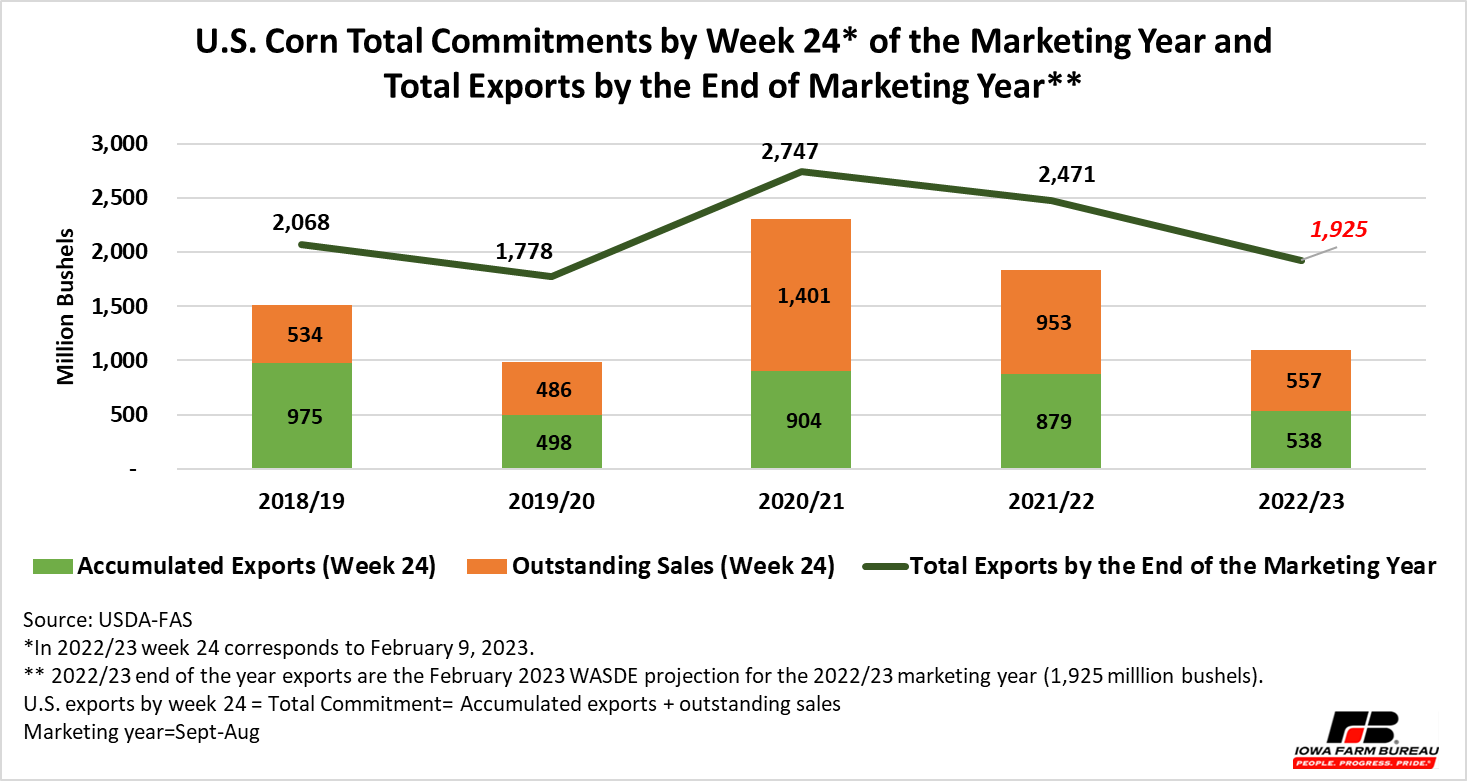

Based on USDA’s most recent trade data, which corresponds to the week ending on February 9, 2023 (week 24 of the marketing year[1]) and published February 16, 2023, U.S. total accumulated corn exports to all destinations were estimated at 538 million bushels, down 38.5% year-over-year (879 million bushels) and 40.5% from the same period in 2020/21 (904 million bushels) (see Figure 2).

Total outstanding corn export sales contracts by February 9, 2023 were reported at 557 million bushels, which represented only 58% and 40%, respectively, of outstanding sales by the 24th week of the previous two years.

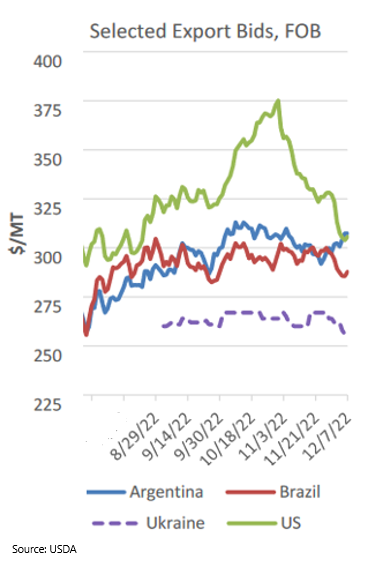

The combination of lower production and the negative impact on grain deliveries to foreign markets coming from the Midwest due to the low water levels in the Mississippi River during the fall of 2022, made U.S. corn prices less competitive (see Figure 1) and resulted in low total commitments (accumulated exports plus outstanding sales). At the peak, U.S. corn export bids were more than $100 per ton higher than corn available from Ukraine.

Figure 1. Selected Export Bids, FOB

The most recent data indicates that total commitments by the 24th week of the current marketing year were estimated at 1.095 billion bushels, which were down 40.2% from last year (1.832 billion bushels) and down 52.5% from the volume during the same time in the 2020/21 marketing year (2.305 billion bushels).

Total commitments by February 9, 2023 made up 57% of the corn export projection (1.925 billion bushels) for the 2022/23 marketing year published in the USDA’s February 2023 WASDE report (see Figure 2). Considering shipments at 538 million bushels, only 28% of projected exports were realized by the 24th week of this marketing year.

In order to achieve the projected volume of exports this marketing year, 49.5 million bushels of U.S. corn have to be exported per week during the next 28 weeks.

Figure 2. U.S. Corn Total Commitments by Week 24 of the Marketing Year and Total Exports by the End of Marketing Year

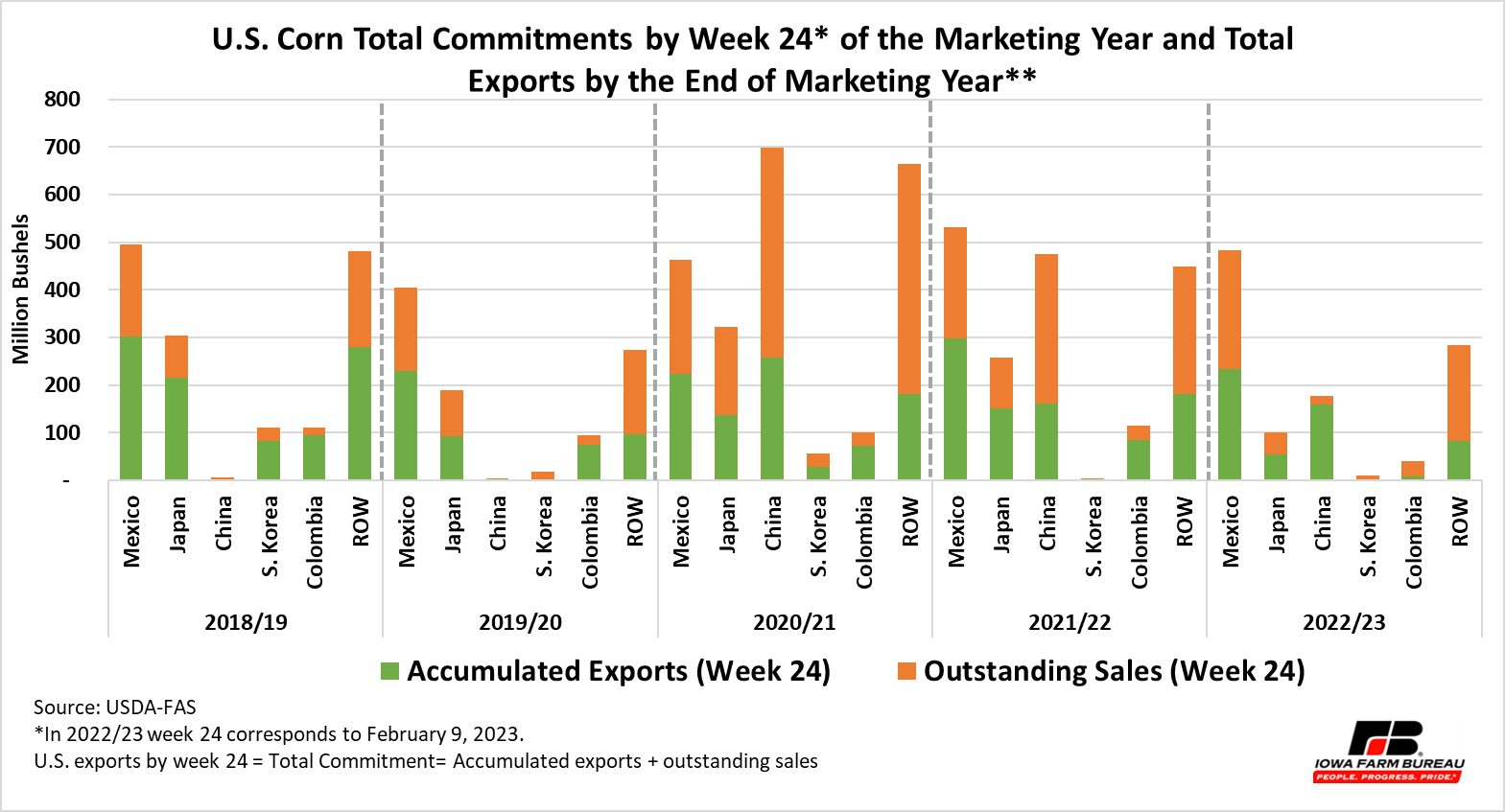

Figure 3 shows corn accumulated exports and outstanding sales by destination. Mexico has been the top market for U.S. corn, except in 2020/21 when China imported large volumes of U.S. corn and became the top market. Figure 3 also indicates that corn total commitments were down relative to the 2021/22 marketing year. Compared with the same week during the previous marketing year (24th week), total commitments were reduced for Colombia (-64.3%), China (-62.9%), Japan (-61.3%), and Mexico (-9.2%) but were up for South Korea (221%).

A note about Mexico corn imports: Mexico had planned to phase out GMO corn imports and the use of the herbicide glyphosate by January 2024. On February 12, 2023, Mexico removed the deadline to ban genetically modify corn for animal feed and industrial use; however, Mexico kept its plan to prohibit use of GMO corn for human consumption (flour, dough, or tortilla made from the grain that is glyphosate tolerant). According to news outlet, the decree also indicated Mexico will revoke authorizations and permits to import, produce, distribute and use the herbicide glyphosate. This plan has been in place since 2020. The transition period would be in effect until March 31, 2024. Considering that between 80% to 82% of Mexico’s corn imports from the U.S. consist of yellow corn for animal consumption, with the remaining imports consisting of white corn for human consumption, this ban would reduce U.S. corn annual exports to Mexico by about 20%.

Figure 3. U.S. Corn Total Commitments by Week 24 of the Marketing Year and Total Exports by the End of Marketing Year

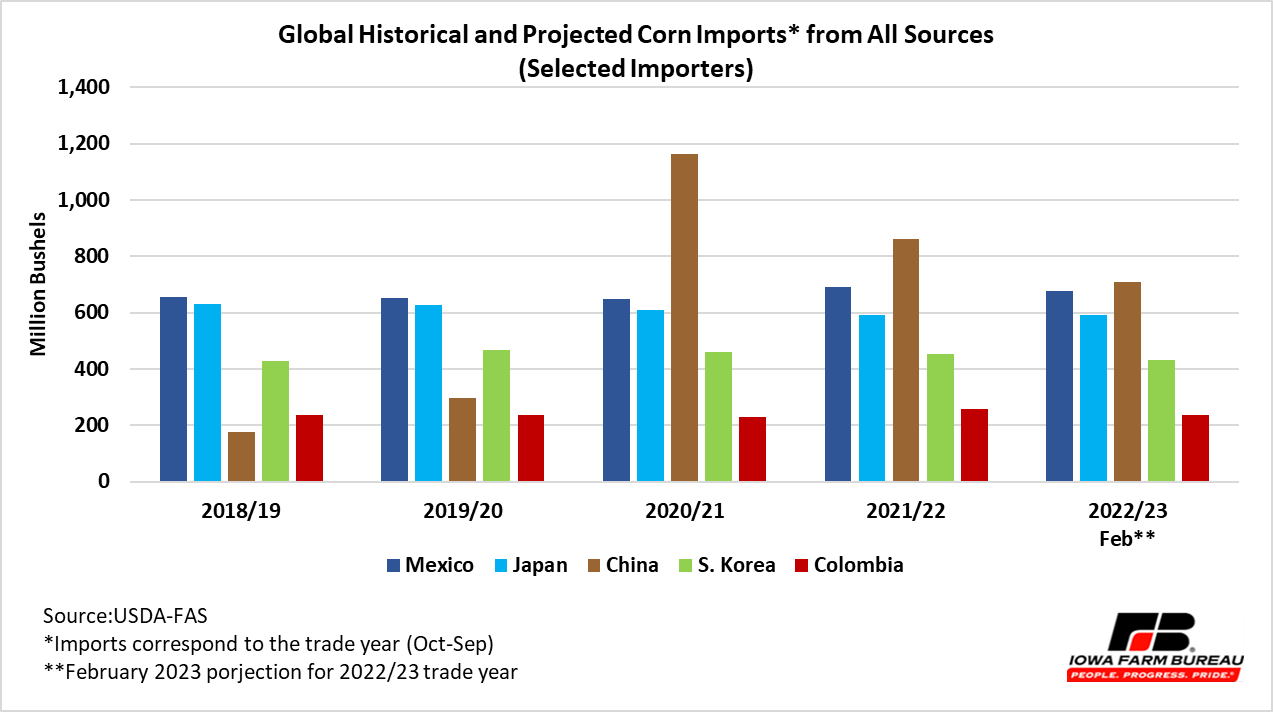

Global corn import projections are down. The latest global corn import projections from all sources during the 2022/23 trade year (October-September) indicate a decline of 6% to 7.179 billion bushels compared with last year. China is projected to reduce its corn imports by 17.7% to 709 million bushels compared with the previous trade year (Figure 4). Colombia, South Korea, and Mexico are forecast to reduce their corn imports relative to the prior year’s trade by 7.9% (to 236 million bushels), 4.5% (to 433 million bushels), and 2.1% (677 million bushels), correspondingly. Japan is expected to keep about the same level of corn imports at 591 million bushels (see Figure 4).

Figure 4. Global Historical and Projected Corn Imports from All Sources (Selected Importers)

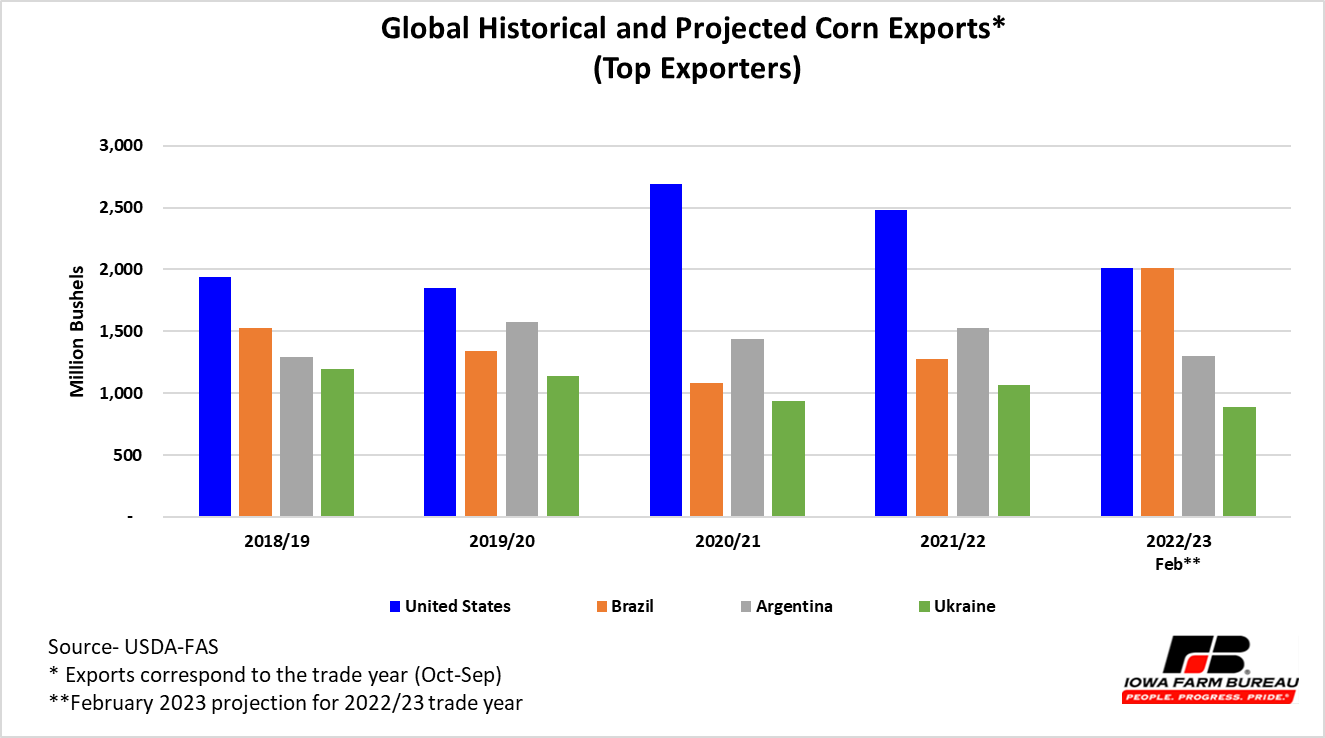

As reported by USDA, major corn importers, particularly China, have kept a high demand for Brazilian corn this trade year. The latest projections indicate that Brazil is expected to reach the same volume of exports as the U.S. during the current trade year (2.008 billion bushels) (see Figure 5). According to USDA, this projection is based on Brazil’s growing production and robust exports during the last six months of that country’s 2021/22 marketing year (March 2022 to February 2023).

Figure 5. Global Historical and Projected Corn Exports(Top Exporters)

[1] Corn marketing year start September 1st.

Economic analysis provided by Patricia Batres-Marquez, Senior Research Analyst, Decision Innovation Solutions on behalf of Iowa Farm Bureau.

Want more news on this topic? Farm Bureau members may subscribe for a free email news service, featuring the farm and rural topics that interest them most!